benlong

benlong

Automation Machinery Manufacturing Industry Tailwinds

A mid-sized electrical manufacturer in Thailand had its manual MCB calibration line replaced with automated testing and assembly equipment in 2023 solely due to the 1.2% defect rate of the manually calibrated circuit breakers, which prompted a warning by one significant European client. After two years of operating the automated line, defect rates dropped to less than 0.05%, production time doubled, and contracts that were once inaccessible for bidding started being targeted. The investment paid off within fourteen months. This specific case exemplifies the ongoing trends that are causing investments in automation machinery manufacturing in all industrial sectors and regions. Labor became expensive and difficult to find where it was previously abundant, quality requirements are becoming stricter, lead times are shrinking, and technologies such as robots, vision systems, and software are already advanced enough for automated lines to stop being experimental projects and be considered rather predictable capital investment projects with clear returns.

Grasping the concept of these tailwinds – their identity, how they work together and in which areas they hold the most power – presents the companies with the crucial question not only of whether or not to implement automation but also of the question of when, in which parts and in what order to do this. The purpose of this guide is to investigate the facts leading to the increase in investments into automation in 2025 and the following years, as well as opportunities from an economic point of view in different industries.

The Structural Tailwinds: Labour, Resilience, and the End of Offshoring

It is not technology that is the biggest driving force behind investments in automation equipment, but demographics. The number of skilled manufacturing workers declines in all major production regions. In 2011, the number of Chinese workers reached its peak and started falling. Japan, Germany, South Korea, and many countries of Eastern Europe experience a similar decline. Those workers who are still employed receive higher salaries and have more job opportunities than their parents. A production facility with manual assembly struggles to find workers now from its neighbors, yet it faces competition from logistics companies, shopping malls, and gig economy providers, which offer workers air-conditioned workplaces and flexible schedules.

According to McKinsley & Company and the Material Handling Institute (MHI), the response to this issue is not automation as a form of replacing workforce but rather using automation to stabilize the workforce. Automation offers manufacturers the ability to perform the repetitive and highly precise assembly operations by employing fewer operators. It can also allow organizations to give their remaining operators work that is of higher quality.

Coming up at the time of the demographic squeeze is a rethinking of the supply chain. With the interruptions caused by years of the pandemic, coupled with geopolitical tensions, and rising shipping costs, many companies are starting to put the trend of reshoring and near‑shoring into action, which means moving production back from overseas countries into North America and Europe. The thing is that reshoring does not have the benefit of low labor costs as the reason for moving production abroad but benefits a lot from productivity and that in a high-wage economy means automation. In fact, companies that emphasize automation as a driver of reshoring according to the Reshoring Initiative have significantly increased during the last years.

The Technology Tailwinds: When the Tools Mature

Modern automated machines are light years ahead of machines from the year 2005. A combination of several technological trends will allow for greater efficiency, flexibility, and affordability of automated assembly and testing:

- Vision and AI‑powered inspection. A camera system capable of learning how to identify a missing micro-screw or tiny crack in ceramics, and which can be taught to recognize a new product within hours instead of being programmed with rules for weeks, has changed the economics of quality control. Vision has become fast and cheap enough to be used at each station on the line instead of limited to just the last inspection point.

- Collaborative and mobile robots. A cobot that operates in cooperation with a human worker, without a protective cage, and can be reconfigured from one task to another in a day, represents a breakthrough in automation investments. Autonomous mobile robots (AMRs), which can travel throughout a factory without fixed routes, have made automated material handling affordable for middle-sized companies that cannot afford installing conveyor systems. The data provided by the International Federation of Robotics (IFR) demonstrate that the number of collaboratively working robots and mobile robots is increasing every year worldwide.

- Digital twins and virtual commissioning. With the advent of software technology, production lines can be virtually designed, tested, and simulated before any metal processing is done. The all-important virtual model analyzes bottlenecks and checks cycle times. It also trains operators on the new system in a virtual environment before the actual production line is installed, thereby decreasing the commissioning process time and minimizing the risks of a faulty line.

- Standardised data and integration. Industrial protocols enable a PLC from one vendor to communicate with a robot from another vendor and a vision system from yet another vendor — OPC UA, MQTT, and PROFINET — have matured to such an extent that multi-vendor automation lines are no longer nightmares in terms of integration problems. Data, traceability, production analysis, and remote diagnostics can easily flow through the line allowing it to be controlled.

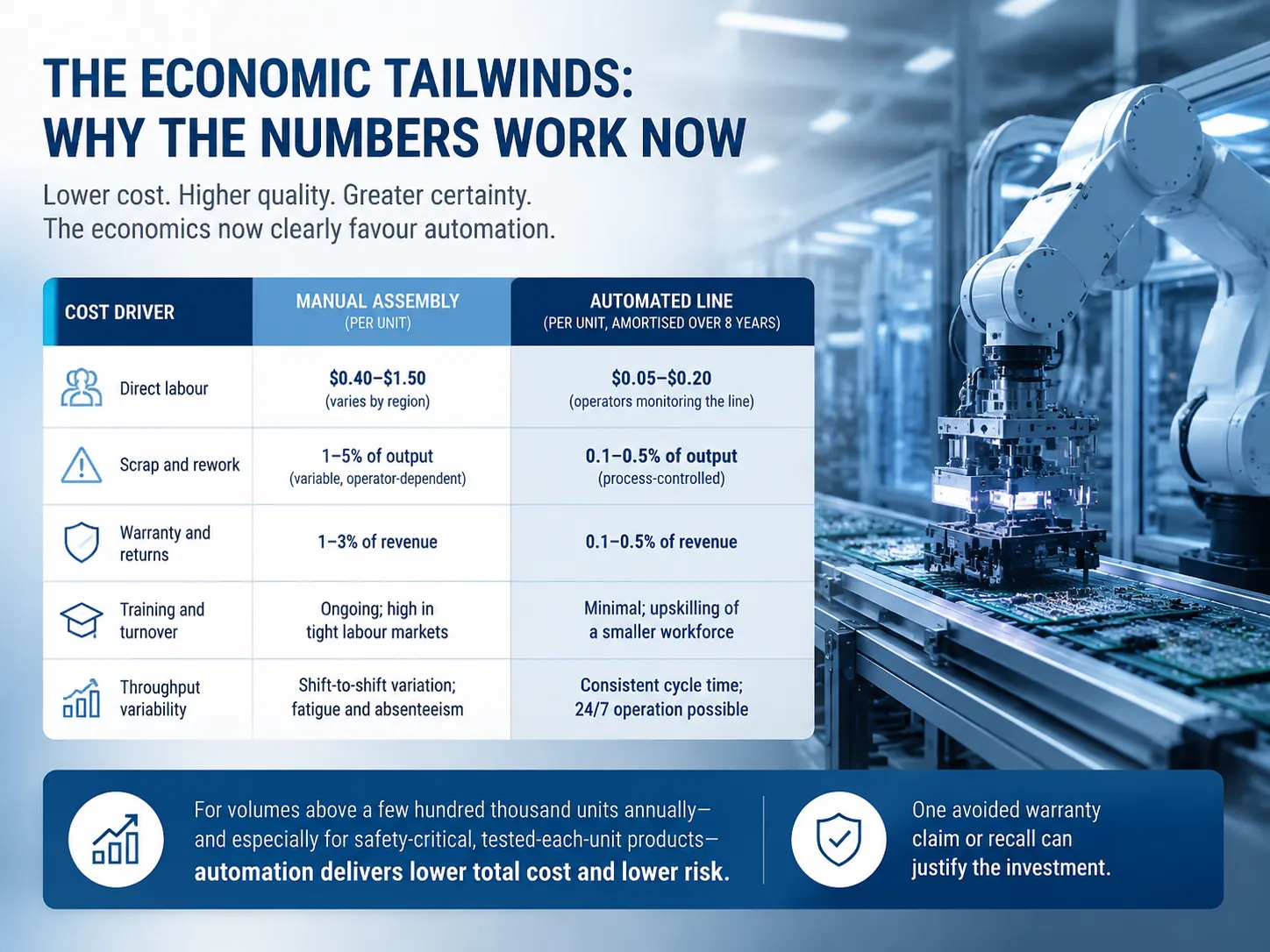

The Economic Tailwinds: Why the Numbers Work Now

An investment in automation machinery is a capital decision, and capital decisions are driven by payback. The tailwinds that are tipping the scales in favour of automation are not just about what the technology can do — they are about what it costs relative to the alternatives.

| Cost Driver | Manual Assembly (Per Unit) | Automated Line (Per Unit, Amortised Over 8 Years) |

|---|---|---|

| Direct labour | $0.40–$1.50 (varies by region) | $0.05–$0.20 (operators monitoring the line) |

| Scrap and rework | 1–5% of output (variable, operator‑dependent) | 0.1–0.5% of output (process‑controlled) |

| Warranty and returns | 1–3% of revenue | 0.1–0.5% of revenue |

| Training and turnover | Ongoing; high in tight labour markets | Minimal; upskilling of a smaller workforce |

| Throughput variability | Shift‑to‑shift variation; fatigue and absenteeism | Consistent cycle time; 24/7 operation possible |

When these expenses are combined for the anticipated lifespan of the machinery, normally eight to fifteen years for an automated assembly and testing line, the total expense per unit manufactured usually favors automation for outputs larger than a few hundred thousand units annually. For items that are safety-critical and tested on an individual basis, such as a circuit breaker, a medical device, or an automotive sensor, the saving achieved from one warranty claim or recall is enough to justify the capital invested in automation. Studies on manufacturing productivity published by Deloitte and other consulting firms often show that automation and digital manufacturing yield double-digit results regarding performance, first-pass yield, and overall equipment efficiency.

Which Sectors Are Catching the Strongest Tailwinds

Investment in automation is highly uneven. The favorable conditions are deepest where the production involves complex processes, quality requirements are strict, and the turnover level is sufficient enough to cover the investments. Among the most promising sectors are:

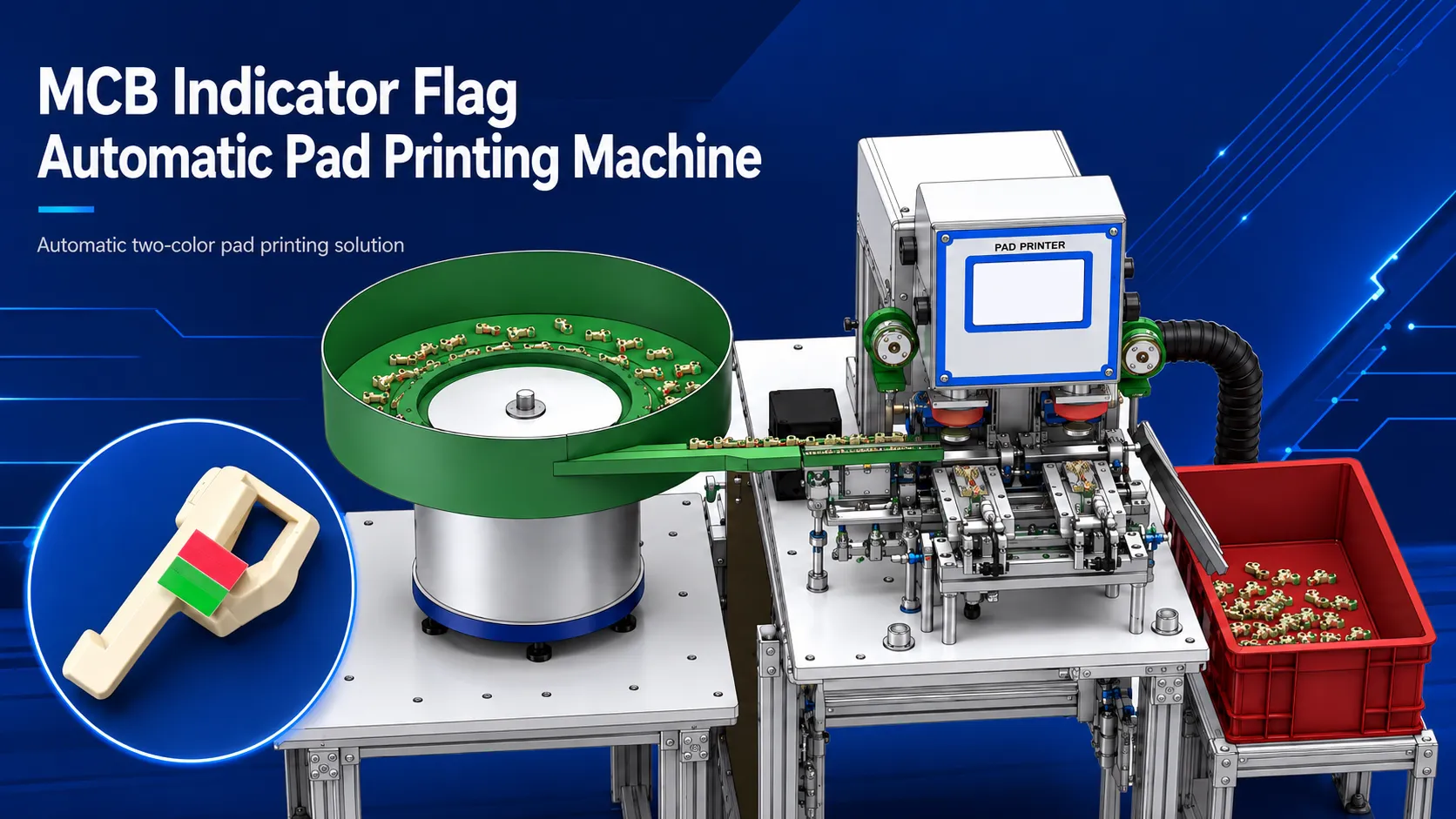

- Electrical equipment and circuit protection. Every miniature circuit breaker, every molded‑case circuit breaker, and every residual current device must be individually calibrated and tested to meet international safety standards. Manual calibration is slow and variable. Automated calibration and testing lines — such as those designed and built by Benlong Automation — calibrate every breaker to its published time‑current curve, record the calibration data against a serial number, and reject any unit that falls outside the specification window. This is not an option for a manufacturer seeking certification for export markets; it is a requirement. Benlong’s MCB automatic assembly line and MCCB automatic production line are configured specifically for this application, integrating parts feeding, assembly, calibration, testing, marking, and sorting into a single, data‑connected flow.

-

- Automotive and electric vehicles. The move to electric cars has brought about a whole new range of assembly processes — including battery module stacking, hairpin stator winding, and high‑voltage connector assembly — which are being automated from the outset. There isn’t any old-fashioned manual lines to replace, though; automation has been inborn in product and process since day one.

- Medical devices and pharmaceuticals. The process of automated syringe filling, inhaler assembly, and packaging of diagnostic kits has a combination of high-performance mechanics with 100% vision inspection and all information about the device history. According to the regulatory demand for traceability, automation has become the default option instead of just an upgrade.

- Food and beverage processing. The automated processes used for filling, capping, labeling, and palletizing are influenced by cleanliness, speed, and difficulties in employing workers in cold and humid conditions. The upsides are the availability of workers and adherence to food safety regulations.

Automation vs. Manual Assembly: When the Crossover Happens

Automation is not suitable for all industries and all manufacturers. The threshold — the quantity of goods and product stability levels at which it becomes cost-effective to introduce automation — will differ based on complexity and labor costs in each region. A simple product with few components and a low likelihood of defects can be made manually up until producing more than 100,000 goods annually. However, for more complex products that feature high risk of defects and strict certification processes — e.g., circuit breakers and contactors — the threshold is often reached far below 50,000 pieces. The decision is not a simple one. A number of manufacturers may want to stick with semi-automated tests and inspections processes, while leaving manual assembly as is. The levels of automation and number of automated workstations will grow in the course of production. Benlong Automation has already thought of a product line to match the gradual integration of automation starting from the installation of semi-automated quality control workstations and allowing for future adjustments to the production line. Our guide on what an MCB automatic testing line is explains the individual stations and how they connect.

The Sustainability Tailwind

Sustainability is an emerging positive force gaining momentum. Automated lines use lower amounts of energy than their manual counterparts — they are not necessarily more efficient machines, but they do produce their products faster, with a minimum of manufacturing waste, and occupying smaller space. The information that is gathered from the automated line is used to prepare sustainability reports that are more and more in demand by customers, investors, and regulators. A producer who is able to prove the energy and material expenses related to the production of each product is going to be in a better position to compete in the environment of carbon borders adjustments and supply-chain emissions reporting.

Frequently Asked Questions

What is automation machinery manufacturing?

Automation machinery manufacturing Automation refers to the designing and manufacturing of systems — assembly lines, robotic work cells, testing methods, conveyors — that accomplishes manufacturing tasks with little or no human intervention. It includes anything from a standalone automated testing bench to an entirely integrated production assembly line.

What is an example of automated machinery?

A typical example of an automatic MCB calibration and testing line. In an MCB calibration and testing line, everything is done automatically and without the intervention of the operator.

Who are the big 4 in the industrial robotics industry?

The name of the “Big Four” in industrial robotics refers to FANUC (Japan), ABB (Sweden/Switzerland), KUKA (Germany and is now part of Midea Group), and Yaskawa (Japan). They are the four top companies when it comes to producing industrial robotic arms, which is used for welding, painting, assembly, and handling materials on a global level.

What are the 4 types of automation?

Fixed (hard) automation for high volume single-product operations, programmable automation for batch processes, flexible (soft) automation for mixed-product operations, and integrated automated systems where the entire factory is data-linked and computer-controlled are the four basic types of automation.

References

- McKinsey & Company — The Future of Manufacturing and Automation. Research on the productivity and quality impact of automation and the labour‑market drivers behind investment.

- Reshoring Initiative — Annual Data on Reshoring and Automation. Data and analysis on the role of automation in bringing manufacturing back to North America and Europe.

- International Federation of Robotics (IFR) — World Robotics Report. Annual data on global robot installations, collaborative robots, and automation density by country.

- Material Handling Institute (MHI) — Annual Industry Report. Data on automation investment trends in material handling and logistics.

- Deloitte — Digital Manufacturing and the Future of Industry. Research on the economic case for automation and the productivity gains achieved by early adopters.

The automation machinery manufacturing industry is riding a set of tailwinds that are structural, not cyclical. Labour is not becoming more abundant. Quality standards are not relaxing. Lead times are not lengthening to accommodate manual processes. The manufacturers who invest in automated assembly, calibration, and testing now — whether a fully integrated line or a single semi‑automated calibration bench — are buying the capacity, the consistency, and the data that will define competitive manufacturing in the decade ahead. Benlong Automation designs and builds that equipment for the electrical manufacturing sector, because the tailwinds are blowing, and the factories that catch them will be the ones still winning contracts when the wind inevitably shifts.